Moving Forward

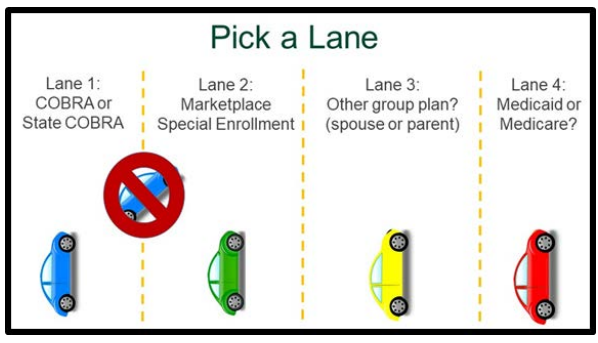

Choosing one of these options is like picking a lane to drive down. As you are comparing these options, remember there are deadlines and rules that apply. In many cases, once you pick a lane, you have to stay in that lane. For example, once you pick COBRA, you cannot switch to a Marketplace plan until the next Marketplace open enrollment period. The new Marketplace plan won’t begin until January 1, so, if you want continuous coverage, you need to keep the COBRA plan until then.

Choosing health insurance is not a one-time activity. You should review your options every year to ensure your plan meets your needs. A plan that met your needs in the past may not meet your needs in the future as your health changes over time. Open enrollment is the time of the year that people can change plans without penalty. The dates for open enrollment will depend on what type of health insurance coverage you have. For example, if you have an employer plan, then it varies, but many employers have open enrollment in the Fall for the plan year to start on 1/1. If you are buying a plan in the state Marketplace, open enrollment in most states is between 11/1 and 1/15. States that run their own Marketplaces may have a longer open enrollment. Starting in the fall of 2026 for the 2027 plan year, Marketplace open enrollment will be between 11/1 and 12/15, but states that run their own Marketplaces may extend open enrollment to 12/31. If you have Medicare, open enrollment is between 10/15 and 12/7 each year.